Understanding Basic Financial Terms Without the Confusion: Financial Terms Explained Clearly

Money talk can feel like decoding another language. But when financial terms explained with everyday context, things click. You deserve to know exactly what those money words mean for you.

Misunderstanding basic finance can lead to expensive mistakes or missed opportunities. Learning the language of money makes budgeting, borrowing, and saving easier. Clear definitions grow confidence and better choices.

This article uses relatable scenarios for each concept. You’ll walk away truly understanding those confusing terms, ready to use them in daily life and long-term planning. Let’s break them down step by step.

Clarifying Balance, Principal, and Interest by Example

When you know the difference between balance, principal, and interest, your statements make sense. This section gives precise definitions and examples you can use today.

Keeping an eye on your account or loan balance means checking how much you owe or have. It changes with every payment, deposit, withdrawal, or fee.

Understanding Principal Amounts in Daily Transactions

The principal is the original amount of money you loan or invest. Every payment toward debt lowers the principal and impacts how much interest you’ll eventually pay.

Imagine paying your credit card. The amount you borrowed is principal. To pay less interest, chip away at that amount directly—use this phrase: “Apply this payment to principal.”

Financial terms explained in plain language: principal is always the starting point for all interest calculations. Keep it low to save on borrowing costs over time.

Differentiating Interest Charges From Other Fees

Interest is the cost you pay to borrow money. Credit cards, loans, and mortgages use rates to set that fee, calculated as a percentage of your balance or principal.

Unlike a flat fee, interest grows as long as the balance remains. Making minimum payments means more of your money goes to interest, less to shrinking the principal.

When reviewing statements, check the “Interest Charged” line. If you see big numbers, pay more than the minimum; that way, you’re tackling both principal and interest.

Comparing How Balances Change Across Accounts

Different types of accounts use balance in specific ways. A checking account lists current funds, while a credit card shows your outstanding debt or available credit.

Example: “My credit card balance is $500, and my checking account balance is $1,000.” Notice how the word balance shifts meaning based on context.

Financial terms explained accurately should always reference what type of account or loan you’re checking, so you know exactly where you stand financially.

| Term | Definition | Typical Use | What to Do When You See It |

|---|---|---|---|

| Principal | Main amount borrowed or invested | Loans, mortgages, investments | Pay extra toward principal to cut interest costs |

| Balance | Total funds owed or available | Banks, credit cards, loans | Check regularly; know if it’s increasing or decreasing |

| Interest | Cost to borrow money, as a percentage | Loans, savings accounts | Shop for low interest rates; pay off balances quickly |

| Minimum Payment | Smallest accepted monthly payment | Credit cards, loans | Pay more than the minimum whenever possible |

| Fee | Flat charge for service or penalty | Accounts, transactions | Ask about fees, and avoid unnecessary ones |

Decoding APR, Compound Interest, and Terms for Smarter Borrowing

Learning about APR, compound interest, and loan terms helps you avoid expensive surprises. These terms shape your costs, so knowing them is protection against confusion.

Financial terms explained in this section show how to compare options and spot hidden costs before you sign any agreement. Take practical notes as you read.

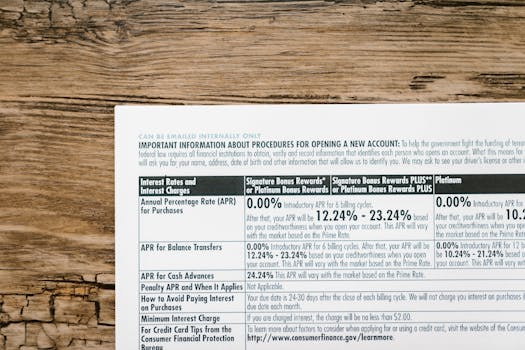

Identifying APR on Paperwork

APR stands for Annual Percentage Rate. It includes interest and most fees, giving the truest cost of credit. Higher APR means borrowing costs more, even if the monthly payment seems small.

When applying for loans or credit cards, always ask “What’s the APR?” This single number lets you compare offers and make choices that favor your wallet.

- Compare APRs before picking a loan, because even a 1% difference can mean hundreds extra over years. Ask for APR in writing, not just over the phone, to avoid surprises.

- Read all APR disclosures in offers. If you see an introductory rate, check how long it lasts and what the new rate will be after the promotion ends.

- Understand that APR mixes interest and fees. A low headline rate with big fees is no bargain, so do the full math or request the full breakdown in writing.

- Write down APR figures from each lender. Compare them on a sheet or online tool. The lowest APR usually saves the most money, especially for large balances.

- If confused, say “Can you explain the APR?” Most reputable lenders provide a simple answer or a written information sheet—avoid any who resist this request.

Financial terms explained: APR is the real deal number to check every time when evaluating credit offers large or small.

Separating Simple Interest From Compound Interest

Compound interest charges you on both the principal and accumulated interest. In contrast, simple interest charges are only on the principal amount over time.

Check credit agreements for how interest accrues. For savings, compound interest means your money can grow faster—but for debt, it can mean paying much more back.

- Choose savings options that use compound interest to your advantage, such as certificates of deposit or high-yield savings accounts—these let your interest earn more interest.

- For loans or credit cards, minimize compound interest charges by paying down balances aggressively. Reducing the principal early means less overall interest paid.

- Understand compounding periods (daily, monthly, yearly). The more frequent the compounding, the faster interest grows on savings—and the larger it piles up on debts.

- Ask your lender: “Is this interest simple or compound, and how often does it compound?” Keep notes for comparison with other offers or products.

- Review annual and monthly statements to track how much interest is added. The financial terms explained section in your agreement tells how calculations work—refer to it regularly.

Choose your savings and borrowing products after clarifying these details each time, and use the actual numbers to plan your payments or investments.

Making Credit Scores and Limits Work for You

Knowing your credit score and understanding your credit limit helps you steer clear of surprises. Used wisely, these facts become tools for financial progress.

Relating Credit Score Ranges to Real Results

Lenders use your credit score to decide approval and terms. A higher score unlocks better rates and terms, while lower scores can mean rejections or higher costs.

Checking your score regularly can help spot mistakes, fix errors, or even catch signs of identity theft. A healthy credit score saves money when borrowing or renting.

Financial terms explained in score reports: “Excellent,” “Good,” “Fair,” and “Poor” translate to real differences in cost and access. Aim to stay above 700 for best results.

Choosing and Managing Credit Limits

Your credit limit is the maximum amount you can borrow on a card or line. Exceeding it hurts your score and triggers fees. Use text or app alerts to track usage.

Spending far below your limit builds a positive payment history. Try: “Keep your card balance under 30% of your limit each cycle” as a habit for stable credit.

If you need more flexibility, call your issuer and ask to increase your limit after showing a history of on-time payments. This can also help your score by lowering your utilization ratio.

Categorizing Savings, Checking, and Investment Accounts

Choosing the right account shortens your learning curve. Each account type has set rules and benefits. Familiarity saves time and keeps your money moving as intended.

Financial terms explained includes knowing where to put your cash for safety, access, or growth. Classifying them helps build an effective financial plan.

Making Checking Accounts Serve Everyday Spending

A checking account acts as a hub for your financial life–paychecks come in, bills go out. Set up low-balance alerts so you avoid overdraft fees.

Keep your debit card in sight during each transaction to prevent mistakes or fraud. Double-check receipts and account updates frequently, especially after large purchases.

Add direct deposit for smoother paydays, and draft a checklist: “Deposit, monitor balance, pay bills, transfer to savings.” This puts your checking routine on autopilot without missing steps.

Identifying the Role of Savings and Investments

Savings accounts give safe, limited access to your cash and usually pay interest. They’re perfect for emergency funds or short-term goals like travel or repairs.

Investment accounts offer bigger potential returns but risk losses. Choose stocks, bonds, or funds when planning for growth. Review account types and set realistic expectations for ups and downs.

Financial terms explained: know the withdrawal rules. Investments may have penalties or delays versus savings, so match account choice to your timeline and comfort with risk.

Spotting Fees, Penalties, and Rewards in Financial Products

Spotting and questioning all possible fees and penalties before signing brings peace of mind. Every account and card has unique extras and gotchas—decode them before committing.

Financial terms explained applies here—scan for buzzwords like “annual fee,” “late penalty,” or “rewards,” and ask for clear numbers in advance every single time.

- Read fine print closely. Fees listed in disclosures or agreements matter. Jot down any charge, plus the trigger, on a sheet for easy review when comparing products.

- Ask explicitly: “What fees apply and when?” If the answer is unclear, press for breakdowns by transaction type and timing, to avoid surprises later.

- Check statements monthly. Highlight unfamiliar charges. Contact the provider right away if anything seems new or unexpected to you.

- Avoid late or overdraft fees by scheduling payments and setting alerts. Two-minute setup today can save big headaches and money going forward.

- Research reward programs by reading the terms on their website. Look for actual dollar value per point or cash back, so you aren’t chasing low-value perks.

Financial terms explained: each number or term has a place in your budget planning. Track everything so you maximize benefits, not costs.

Updating Your Language for Modern Money Management

Adapting to today’s financial tools and lingo puts you one step ahead. Apps, websites, and digital statements all use familiar terms you’ve seen in this article.

Practice using these financial terms with your real numbers to stay sharp. Saying, “Here’s my balance, interest, and APR,” keeps you engaged and in control, not lost in jargon.

Scenario: Asking for a Loan Summary In-Person

Walk into a bank and say, “Can you explain the principal, balance, APR, and total fees on this loan?” Take notes for each term—this script makes you sound prepared.

Notice your body posture: upright, attentive. If you notice unclear answers, pause and ask, “Where is this fee shown in writing?” That’s how to avoid being steamrolled by technical jargon.

Financial terms explained is your right as a customer. Repeat back what you hear and don’t sign unless satisfied. Real understanding builds trust and saves money.

Adopting Digital Banking Language for Clarity

Mobile banking dashboards let you see snapshot terms such as “available balance,” “current balance,” and “pending interest.” These mean different things based on transaction timing and account setup.

Tap each term to see definitions or help screens. If the text isn’t clear, call the support line and say, “Explain this financial term as you would to a beginner.”

Financial terms explained: Don’t accept confusing answers. You deserve plain language whether banking on your phone, in person, or reviewing an email statement. Consistency makes learning stick.

Taking Your Financial Language Into Daily Life: Next Steps

We’ve covered the financial terms explained most essential to your money life. Use these definitions when checking statements or comparing offers, and refer back whenever anything seems unclear.

Every time you use your understanding, you reduce the risk of surprise fees and set yourself up for better financial outcomes. The language of money is now a tool, not a barrier.

Take a minute to find one term from today’s article you’ll double-check in your next transaction. Small shifts today make big changes over time. Let these financial terms explained drive your new habits.